The value of tomorrow is realized in partnership with Zonebourse.com

As its name suggests, AMS-Osram is a relatively recent marriage between two companies that haven’t had time to think about their new names yet. The Austrian AMS has indeed bought the German Osram in 2020 for 4.6 billion euros, with a view to creating a major player in photonics and sensors, a very specific branch of the vast semiconductor industry. The transaction was made under the nose of the investment funds which eyed Osram, the former lighting division of Siemens.

At first glance, uniting a specialist in sensors and a manufacturer of light bulbs may seem incongruous. But the industrial logic is there, as sensors and light sources are increasingly combined into a single solution that includes a transmitter, an optical path, a receiver, driver ICs and application software. . In any case, it is in these terms that AMS explained it in 2019 to support its acquisition offer. The duo prides itself on being the only player in the world to have a complete offer in its field.

Apple Addiction

Despite this enticing promise, the honeymoon was cut short. It indeed coincided with headwinds for both companies. At AMS, it was falling revenue from Apple that put the company under pressure. The Austrian has long displayed a very generous stock market valuation thanks to its status as the Californian’s benchmark supplier. At their peak, orders from Apple generated almost half of the revenue of AMS, which supplied the iPhone with its 3D Face ID and ambient light sensors for display management. The two companies remain in business, but the technological developments of the smartphone have largely planed the juicy original contract. On the Osram side, activities were sluggish at the time of the merger, with strong competition on low-margin products and a bumpy automotive market. Assessment of the operation, the share price of AMS-Osram collapsed and the current enterprise value, approximately 4.4 billion euros, is lower than that of AMS in solo in 2019. In finance , it’s almost a textbook case of value destruction.

But the group begins to see the end of the tunnel. Osram is in the process of selling its most fragile assets, while AMS has diversified its sources of income to reduce its dependence on Apple. The first effects are already visible. The automotive division has gained weight, to represent half of the revenues of the first half of 2023, reducing the share of the consumer branch, the one that includes smartphones, to 18%. The third activity, “industry and medical”, remained stable at 31%. Above all, management was able to raise its forecasts at the end of July, which is the first good news that the market can eat for several quarters. Improved results should follow. Analysts believe that free cash flow will become positive again in 2024 and that the situation will normalize in 2025, six years after the publication of the banns.

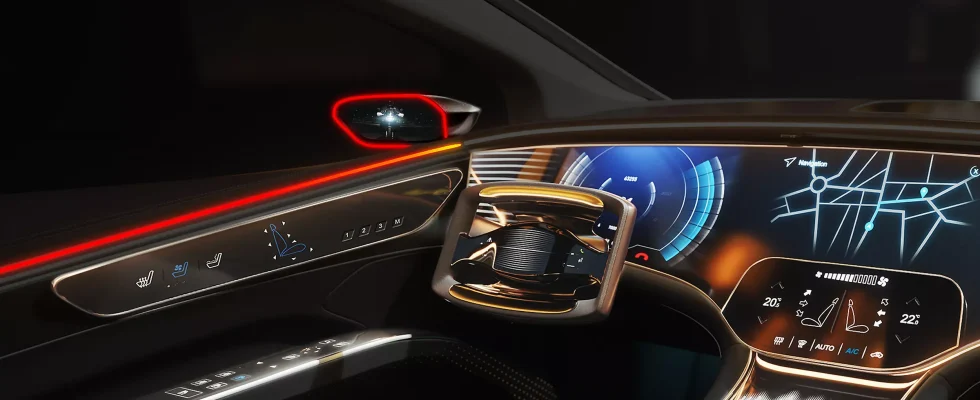

Exhibition of the vehicle of the future

AMS-Osram is clearly what financiers call a “special situation”, which is akin to the “must prove itself” report cards from our childhood. The company is emerging from a painful merger and has just begun its operational recovery. And if the dependence on Apple has improved, it still has to refinance a major debt maturity in 2025. Its strengths? Strong exposure to the theme of the vehicle of the future, thanks to essential solutions for lighting, human-machine interfaces and autonomous driving. Less reliance on the volatile consumer electronics sector and strong market shares in the demanding industrial and medical fields. And of course, to top it off, a price that not so long ago was flirting with ten-year lows.