It is difficult to invest in stocks today as growth prospects are uncertain. Certainly, the Paris Stock Exchange posted excellent results in 2023, with an increase of 16.5% in the CAC 40. But precisely: can such performance be repeated in 2024? On the contrary, many savers fear a decline in the market and, therefore, wonder what to do.

Let them rest assured: it is possible to benefit from well-paid, secure investments for a few months, while waiting for the right time to return to the stock market. These risk-free and liquid products – you have to be able to get out of them quickly to invest when an opportunity arises – yield around 3% per year, a level not seen in ten years. The successive increases in key rates decided by the European Central Bank (ECB), which took place between July 2022 and September 2023, brought the deposit rate to 4%, giving new color to short-term investments. Therefore, the planets should remain aligned as long as central bankers do not decide to lower them. “This should not happen before the end of the first half of 2024,” indicates Philippe Crevel, director of the Circle of Savings. Savers therefore still have a few months ahead of them to benefit from an attractive return on their savings without risk. The decline should then be gradual.

© / The Express

The right strategy therefore consists of favoring the Livret A and the Sustainable and Solidarity Development Livret (LDDS), the yield of which is frozen at 3% until January 31, 2025. “They must be filled as a priority up to their respective ceilings. , i.e. 22,950 euros for the Livret A and 12,000 euros for the LDDS”, advises Maxime Chipoy, the president of MoneyVox. These products are in fact the most profitable on the market for investing your money over a year because they are exempt from taxes and social security contributions. “The good news is that their real yield, that is to say after inflation, will become positive again during the year 2024,” underlines Philippe Crevel. The Banque de France is in fact counting on a price increase of 2.5% this year, after 4.9% in 2023. Low-income households should instead turn to the popular savings booklet (LEP), yielding 5% since February 1. It is also not subject to tax or social security contributions and it is now possible to contribute up to 10,000 euros.

Life insurance is recovering

Beyond the regulated savings ceilings, we must look for other solutions, often less remunerative. Certainly, the return on life insurance funds in euros is recovering: it should be around 2.5% in 2023, before social security contributions, and some savers will be able to obtain much more with the bonuses paid by insurers to their clients investing partly in units of account. But this support cannot replace the Livret A since it does not benefit from the same liquidity. It is better to look at traditional (taxable) bank accounts, which can often collect up to 10 million euros.

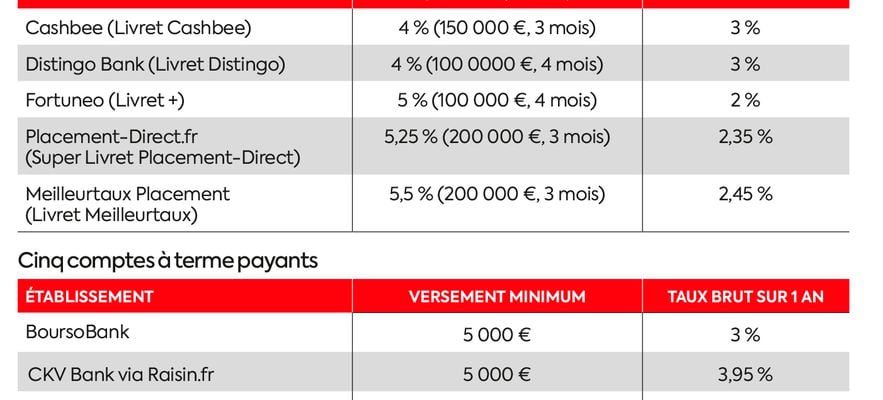

Good news: online savings players have been engaged in a rate war for several months, in which the big winner is the saver. “The savings accounts of network banks, on the other hand, are very disappointing, with rates often between 0.10% and 0.50%,” notes Maxime Chipoy. Elsewhere, it is possible to find offers, reserved for new customers, at 5%, or even 5.50% over three or four months. Once this period has passed, the standard rate applies, amounting to 3% for the best. Please note: this increased rate only applies to a limited amount: 20,000 euros at BforBank, 150,000 euros at Cashbee or even 200,000 euros at Placement-Direct.fr and Meilleurtaux Placement. “Our booklet is more profitable than the booklet A over a short investment period,” underlines Gilles Belloir, the general manager of Placement-direct.fr. Over three months, the net return on single flat-rate direct debit thus comes out to 0.92% (5.25% for three months – 30% taxes) compared to 0.75% for the A booklet (3% over three months). Individuals with a large sum to invest for a few months, for example from the sale of real estate or a donation, have an interest in shopping around the market to choose the best offer because these are regularly renewed.

If you have a specific investment horizon, twelve or eighteen months, for example, you can also look into term accounts, the rate of which is fixed once and for all when subscribing. This is slightly higher than that of the booklets in order to compensate for the blocking of funds. Because if it remains possible to exit a term account early, the operation then results in a penalty on the yield. “It is better to spread your savings over several term accounts maturing gradually, for example at twelve, eighteen and twenty-four months, in order to avoid having to exit early,” advises Maxime Chipoy. Thus, Distingo Bank currently offers a return of 3.50% on its one-year term account, 3.20% over ten months and 3% for its savings account. “We no longer currently offer term accounts longer than one year because market interest rates are lower for longer durations,” explains Sarah Zamoun, head of the Distingo activity. Two-year interest rates are in fact lower than one-year interest rates. Network banks also offer attractive rates to their customers, but often for significant deposits, above 50,000 euros.

As for money market funds, they are making a comeback after seven years of negative performance. They show an average increase of 3.37% over one year as of January 2, 2024 according to Morningstar, which makes them a good replacement solution for regulated savings accounts, once their ceilings are reached. Housed in a securities account, their winnings are subject to the single flat-rate deduction of 30%. But these supports can also be subscribed to in different tax envelopes including life insurance and they are then subject to the related taxation.

In any case, be sure to choose a product whose management fees are as low as possible (they amount to 0.15% on average) so as not to weigh too much on performance. Finally, note that the outlook remains favorable for 2024. Money market funds are in fact invested in securities issued by companies and banks, the return of which is indirectly linked to the level of the ECB’s key rates.

The PEL, an option not to be neglected

Although it is less well paid than the Livret A, it has other advantages.

Home savings plans (PEL) opened since January 1, 2024 yield 2.25% gross, or 1.57% net after deduction of the single flat rate deduction of 30%. Certainly, this rate remains well below the 3% net of the Livret A and LDDS. But the PEL has an advantage: its rate is fixed for the next fifteen years, while that of other regulated investments varies over time. In two or three years, the return on the Livret A will perhaps be lower than the current level of the PEL.

The good strategy therefore consists of opening a plan to set a date, if you do not yet have one, even if it means only placing the bare minimum there at first. How much ? You must pay 225 euros upon opening, then at least 540 euros per year, i.e. a savings effort of 45 euros per month.

Please note, this product is not liquid: any withdrawal results in its closure, so you should only invest amounts that you are certain you will not need. After a savings phase of at least four years, the latest generation of PEL will allow you to borrow to finance your main residence, at a rate of 3.45%. It is difficult to know whether this rate will be attractive when the day comes, but the history rather speaks in its favor.

An article from the L’Express special report “Investing in 2024: the right strategies for an uncertain environment”, published in the weekly on February 15.

.