(Finance) – Italy received EU recovery funds according to plan, but spending falls short of initial expectations, a problem that is set to worsen as capacity constraints on the country’s local authorities hold back projects of investment. Slow progress in the use of approved EU funds could also jeopardize future EU disbursements, as these will increasingly depend on the government’s ability to implement investment projects (“targets”) rather than on the implementation of reforms (” milestones”). Investments are also crucial to boosting Italy’s growth potential, which is vital for sovereign debt sustainability. These are the main findings that emerge from the comment by Scope Ratings entitled “Italy: the recovery plan suffers delays in the investment phase, while the burden falls on local authorities”, curated by Alvise Lennkh-Yunus, Giulia Branz and Alessandra Poli.

THE delays in implementing projects using Recovery and Resilience Facility (RRF) funds of Italy by 191.5 billion euros, equal to 10.8% of GDP in 2021, represent – reads the report – a growing risk for the prospects for economic growth, which is essential to support the high public debt of the country and maintain its BBB+/Stable credit rating.

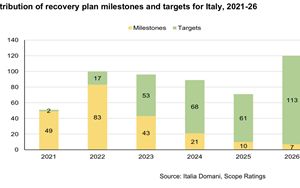

So far, Italy has achieved all the necessary milestones and objectives to receive the funds foreseen by the European Commission for 67 billion euros. These disbursements were conditional on the implementation of judicial, public administration and competition reforms. They will come this year a further 37 billion euros will be released if the 43 goals and 53 objectives set are achieved. However, theThe Italian government spent just 5.5 billion euros in 2020-21, a figure – underlines Scope Ratings – well below the original plan of 18.5 billion euros, while the 2022 expenditure was 15 billion euros compared to the 28.7 billion euros initially foreseen. The slower-than-expected implementation of investment projects is likely to challenge the government’s expectation to raise Italy’s public investment rate to 3.7% of GDP by 2025 from 2.5% of GDP in period 2010-20 compared to an EU average of 3.1%. Slow progress in the use of approved EU funds could also jeopardize future EU disbursements, as these will increasingly depend on the government’s ability to implement investment projects rather than on the implementation of reforms.

Indeed, the low disbursement of EU funds received to date is common among some of the largest recipients of RRF funds, including Greece, Portugal, Spain and Croatia. This is due to the energy crisis, higher raw material costs and supply chain disruptions. In such a scenario, the EU – speculates Scope Ratings – could grant further flexibility regarding the timing and selection of projects for recovery plans in all EU Member States.

With an absorption rate of the European Structural and Investment Funds of 60% in 2022 for the funds allocated in the period 2014-20,

LItaly is third last in Europe ahead of Slovakia (59%) and Spain (54%) and is well below the EU average of 75%. This reflects – according to the Scope Ratings analysis – the lack of technical skills in public administrations, together with the slow adaptation to the fast-track procedures for planning and procuring projects. The Italian government has called for a postponement of the 2026 deadline for spending RRF funds. Infrastructure projects worth around €40 billion are at risk of not being implemented by 2026, and funds not spent in 2020-22 have been reallocated into 2023-26, further increasing the likelihood of delays.

The Regions, Provinces, Municipalities, Metropolitan Cities and other Italian local authorities – which manage a total of around 66 billion euros – have a crucial role to play in realizing the large investments envisaged by the recovery funds. More than half of these resources (40 billion euros) will be assigned and managed directly by the Municipalities, making them the main implementers of the Plan projects. A complete overview of the implementation status of individual investment projects in Italy or in the EU as a whole is not yet available, even though preliminary data show that Italian municipalities have presented around 70,000 projects by the end of 2022, for a value of 29.5 billion euros, out of a total of 40 billion euros assigned to them.

The Local societies, especially in the southern regions which are expected to receive at least 40% of the funds, are facing considerable difficulties in completing tenders and obtaining third party authorisations. Cost savings over the past decade have led to nearly 30% headcount cuts in the municipal sector and have contributed to an aging civil servant workforce – with an average age of over 50 – limiting government capacity premises to adapt to new technologies and procedures.

The government is therefore seeking to strengthen local administrative capacity by streamlining bureaucratic and recruitment procedures and encouraging the hiring of external firms and technical assistance consultants, among other initiatives.

Supporting these efforts – it is highlighted in the commentary – is essential for the successful implementation and future maintenance of investment projects in the coming years to ensure a lasting contribution to economic growth and the sustainability of the Italian debt. Furthermore, the successful implementation of Italy’s substantial recovery plan is important to foster confidence among EU Member States for any future discussions on EU-level tax policies and frameworks.