(Finance) – In December 2022, the NPE market is facing a situation of general expectation and ready to face potential changes in the face of: the amount of bank stocks of non-performing loans in continuous decline, reaching the lowest levels in recent years now mature and consolidated NPL transaction market, thanks to increasingly tested and standardized processes and increasingly present specialized operators evolving judicial world thanks to government investments in the digitization of procedures, encouraged by the funds of the PNRR. This is the picture that emerges from fifth edition of the NPE Observatory created by CRIBIS Credit Management – company of CRIF Group specialized in the management of Collection and NPL management processes – which aims to provide an overall and updated view of the NPE market.

“The scenario of global socio-economic instability and the phenomena linked to inflation and the increase in interest rates – comments Andrea Capellini, analytics manager of CRIBIS Credit Management – require financial players to pay close attention to non-performing loans and their monitoring in order to be ready to deal promptly with any future developments”.

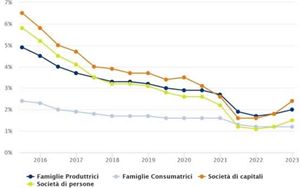

Trends in the credit risk of households and businesses – 2022 saw a turnaround in credit risk with four consecutive quarters of increase. Considering the uncertain macroeconomic scenario, 2023 is expected to be characterized by a trend that will continue to grow as regards bank default rates. Compared to 2021, Consumer Families: the percentage remains unchanged at 1.2%; Producer Households: from 1.7% in December 2021 to 2% in December 2022 (+18% YoY); Partnerships: from 1.1% in December 2021 to 1.5% in December 2022 (+36% YoY); Limited companies: from 1.6% in December 2021 to 2.4% in December 2022 (+50% YoY). With reference toanalysis of NPE (Non Performing Exposure) stocks 2022 confirmed the gradual shift of market attention from non-performing loans to loans classified as UTP (Unlikely To Pay or unlikely to pay) and Stage 2 (performing loans showing a significant increase in credit risk). As for i credits classified in Stage 2, having reached over 263 billion and representing around 13.1% of total bank loans, the most significant percentage of this exposure can be connected to joint-stock companies which account for almost 70% of total loans in this state of initial alert. THE riskier manufacturing sectors constructions and infrastructures (24.4% of exposures), together with services (18.8% of total exposures) with logistics, food & beverage registering the greatest increases. Conversely, the sectors with a small share of exposure remain those of oil and gas extraction and chemical and pharmaceuticals. As regards the unlikely to pay (UTP), the analysis confirms the trends of recent years, confirming again among the riskiest sectors those related to the real estate and construction sectors, entertainment (accommodation, catering and travel agencies) and commerce. The situation of uncertainty linked to the increase in interest rates, inflation and the issue of liquidity will prove to be crucial events for companies in 2023, thus becoming a key year for assessing the effective stability of the country’s real economy .

Stock and NPE market: sales – To analyze the dynamics of the NPE Stock, the analysis in partnership with Credit Village is confirmed, focused on the trend of loan assignments. At the end of 2022, transactions were carried out for around €34 billion, of which 83% related to NPL portfolios and only 17% to UTPs. This is the lowest value in the last 6 years. Furthermore, with reference to the type of market, for the first time there was a higher number of transactions on the secondary market than on the primary market (51.4% of the transactions representing 20% of the gross book value sold during the year). This too represents an important turnaround that marks a probable new path for future years. “The increase in interest rates and the consequent cost of funding, combined with the negative effects of inflation on the entire economic system, – he says Roberto Sergio, CEO of Credit Village and Scientific Director of the NPE Market National Observatory – prompt investors and debt buyers to urgently carry out a precautionary review of the valuation and pricing models of NPE portfolios. Since June 2022, coinciding with the decision to raise interest rates by the ECB, we have noticed a progressive contraction in sales transactions, especially on the primary market. 2023 will therefore be a further test for the entire credit industry which, after the pandemic shock, successfully overcome, will have to demonstrate its full degree of resilience and maturity in facing the new scenarios. One thing is certain: it will be increasingly difficult to find the matching on sale prices, influenced by the higher expectations in terms of IRR by investors”

Extrajudicial recovery – In 2022, according to the analyzes of CRIBIS Credit Management, the performance of out-of-court recovery proved to be down compared to the previous year, especially for the unsecured loans sector. This phenomenon, visible through the analysis of the lower rates of return to performing both for consumer households (-7% 2H 2022 vs 2H 2021) and for companies (-10.0% 2H 2022 vs 2 °H 2021), demonstrates a renewed phenomenon of market risk. This risk event is linked to consumer credit (for the retail component), to liquidity loans for the maintenance of the business (for the corporate component) and to the end of the moratorium and pre-amortization periods which guaranteed the subsidized finance loans. The indicator for loans secured by real estate is substantially stable. The improvement rates from a situation of initial deterioration of loans (Stage 2) are stably lower for the unsecured loans segment (-12.5% 2022 vs 2021) and secured by real estate (-9% 2H 2022 vs 2 °H 2021). It will be necessary to pay particular attention to risk monitoring and early collection activities to avoid dangerous further slides towards more serious situations.

Judicial procedures – In 2022, more than 300,000 new proceedings were registered in the field of enforcement and insolvency procedures, recording a slight increase (+6.5%) driven by securities enforcement procedures, which increased by 10% reaching almost 266,000 new foreclosures. On the other hand, real estate executive procedures (about 33 thousand new procedures, down by 8% compared to 2021) and insolvency procedures (about 7 thousand procedures, down by 22%) are decreasing. However, the back logs are decreasing in all sectors with greater relevance for executive procedures (-24.6% for real estate executions and -22.7% for securities executions) than for insolvency procedures (-3.6%) .

Real estate executions – If from the point of view of stocks, the disposal of real estate executions and the number of judicial auctions continued a positive trend also in 2022, as far as the performance of the Italian courts is concerned, there are still no significant improvements or a return to values similar to the period pre-pandemic. In fact, from the point of view of the timing for real estate sales, the figure is increasing (from 5.2 years in 2021 to 5.6 years in 2022) with increasingly worse performances in the centre-south than in the north. However, the times for allocating the sums after the award have improved with an average drop of around 30%, falling below the year of time necessary for the definitive closure of the procedure. On the other hand, the average recovery rates given by the judicial value (about 64% of the real estate value according to the CTU’s appraisal) remain stable, with residential properties still proving to be the most attractive and transacted category within the Italian market.

Judicial settlements – There will no longer be talk of bankruptcy but of judicial liquidation of assets: this is the great news that brought about 2022. From the point of view of the trend, on the other hand, the general decline in new registrations of procedures is confirmed, with around 7 thousand procedures registered per year in the Italian courts, reaching the historic lows recorded in 2008. The average time to complete the liquidation is stable (about 6 years on average).