One part of the tax form isn’t always obvious and it can be tempting not to report it quite correctly.

For many taxpayers, completing the tax return is a real headache. There are many boxes that must not be forgotten and, sometimes, the tax assistance notice does not really help to see things more clearly. Each year, around a million French people must complete a very specific line of the form. However, it is not always easy to navigate because the statements are not necessarily explicit and the administration recognizes that this is even one of the “most frequent” errors in the declarations.

To avoid receiving a message from the DGFiP, or even a tax adjustment if a fine is imposed, it is preferable to look carefully at this subject: alimony. Nearly a million are paid each year, according to the Alimony Recovery and Intermediation Agency (Aripa). The most common case concerns the parent who does not have permanent custody of their child(ren) and who thus pays financial assistance to the other parent to contribute financially to daily costs.

Giving money to your ex-partner who is raising the children helps lower your taxes. For the person receiving the pension, on the other hand, it must be declared to the tax authorities. And while it may be tempting not to say anything to the tax authorities, the latter can very easily track you down. It is therefore better to be transparent and consistent with the person who helps you.

Indeed, when a taxpayer pays alimony, he must enter it in the “Your expenses” section, “Deductible expenses” section:

- In box 6GU for the minor child(ren) assisted

- In box 6GP for the minor child(ren) assisted by court decision before 2006

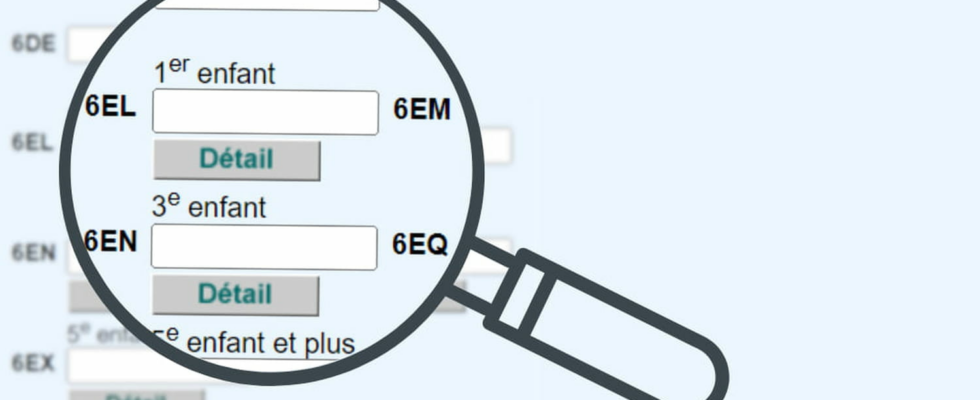

- In box 6EL and following for each adult child

- In box 6GI and following for each adult child by court decision

Above all, it is mandatory to click on the “Details” button below the boxes mentioned above in order to provide the identity of the person receiving the alimony. This is how the tax authorities then carry out cross-checks to check that the declarations are consistent.

For their part, the person receiving the pension must follow several steps to declare it. When the page “Select the sections you wish to appear below”, you must check the box “Pensions, retirements, annuities, life annuities for payment”. On the next page, simply fill in box 1AO “Alimony received” with the amount received during the year.

It should be noted that in both cases (giver or recipient of a pension), you must enter in your declaration the amounts paid/received between 1er January and December 31, 2023. Be careful not to take into account the start of 2024.