The vitality of American technological innovation is historically based on an ideal sequence: the manna of the military during the Cold War fertilized the formidable intellectual breeding ground of universities and research centers of excellence. Then, in the 1970s, the emergence of venture capital provided this entire ecosystem with the fuel necessary for its vitality. However, it is this last cog that is about to seize up today, without anyone really knowing if the financing of private innovation in the United States is simply cold or if it is entering a period of glaciation. sustainable.

The current crisis actually has its roots in the financial meltdown of 2008. Immediately after the bank failures, the financial system entered a potentially devastating catalepsy for the global economy. The first instinct of the American financial authorities was to launch a vast operation to buy back certain securities held by the banks, including the most caricaturally speculative bonds which had been at the origin of the crisis, in the hope of unblocking the situation. But the banks did not play the game, and contented themselves with rebuilding their profitability without reopening the floodgates of credit.

Hence the second weapon deployed by the American Federal Reserve: a historic decline interest rates. Between June 2007 and January 2009, the base rate fell from 5.51% to virtually zero. The period which then opened, ten years long, was that of “free money” or “easy money”, according to the established term.

The era of free money

American tech jumped at the chance to invest massively. This is the time when Amazon is developing its immense logistics infrastructure with its robotic warehouses, its fleet of cargo planes and ships that stuff the West with all these goods from China. Google and Microsoft are building data centers, pull undersea cables across the oceans to connect all these markets. Valuations are soaring. WeWork promises a valuation expressed in trillions of dollars.

But this free money, companies also use it to buy back their own shares in order to support the price. This appeals to shareholders, but also to employees stuffed with stock options. Absolute champion of these buybacks, Apple, which over the past five years has repurchased more than $400 billion of its own stock. During this decade with interest rates close to zero, American companies will spend 6,000 billion dollars in share buybacks, or the equivalent of three times the French GDP. All of this leads to a cycle of affluence disconnected from reality and reinforces inequalities.

This crazy prodigality where debt is king also benefits venture capital, the financial pump of the system. A fund of venture capital (VC) works as follows: large so-called institutional investors – pension funds, insurance companies, wealthy universities, family fortunes – invest in venture capital firms. They constitute what are called LPs, for limited partners. Their requirement towards the firm of venture capital ? Build a portfolio of companies leading to spectacular capital gains. In practice, the firm of XY Ventures will raise a fund of 600 million over a period of several years, and calls for funds from LPs will be made according to needs, that is to say equity investments in start-ups. This notion of regular calls for funds is important for the future, we will come back to this.

SVB lubricant

Enter the Silicon Valley Bank and its forty years of assiduous lubrication of the system. “Everyone had to be at the SVB, says an entrepreneur, because it was much more than a bank. As soon as you opened an account, you were entitled to a line of credit and the introduction to a network of influence exceptional in its scope and quality. The bank was monitoring his businesses; they reviewed all my decks [NDLR : présentations aux investisseurs]…” The SVB, the 16th American bank, supported more than 50% of Californian start-ups. Suffice to say that it was overexposed to risk: that of its customers, fragile by nature, and that of its own investments in Treasury bonds. term and, again, in highly speculative financial instruments, all of which lost value rapidly as interest rates began to rise.

When start-ups began to reduce their savings in the face of a business slowdown, as money from VCs – also SVB clients – became scarce, entrepreneurs needed to withdraw their cash. A deadly scissoring effect ensued. To save the ecosystem, the Federal Bank Deposit Insurance Fund (FDIC) even went so far as to compensate all SVB’s deposits, whatever the amount, forgetting the guarantee limit of 250,000 dollars, before arranging for the takeover of SVB’s assets by a family bank.

This eagerness of the American government to save the SVB shows the shift in the notion of too big to fail (too big to fail) towards a principle in the broader sense of “too important for an ecosystem to be abandoned”, is surprised Thierry Philipponnat, former international banker, now chief economist for the NGO Finance Watch in Brussels. “It is interesting to see all these tech libertarians, who advocate absolute decentralization, including through highly risky tools like cryptocurrencies, suddenly asking that the federal state come and save the tech bank. the perfect illustration of the scheme where profits are privatized and losses state-owned.

This sends a very bad message to the American financial system, which will feel freed from all management constraints, since the certainty sets in that in the event of a hard blow, the State is there.” The former president of the FDIC, Sheila Bair agrees, declaring in an interview: “The American business community has taken a liking to bailout (rescue). They invoke the survival of capitalism, me, I see it rather as a threat.” For her, it is the implicit permission to resume the “speculative orgy” (according to the expression of a former Federal Reserve) as soon as that the conditions will allow it, with the systemic risk that goes with it.

The “whatever it takes” US version

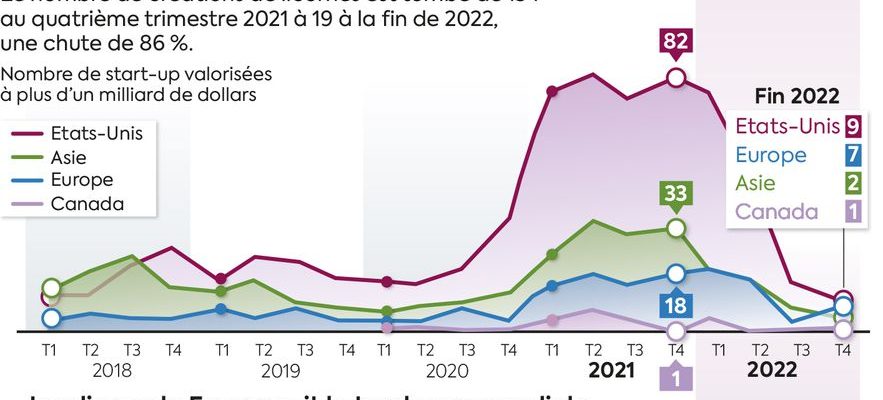

And now ? At the start of the year, the fundamentals of innovation financing in the United States – and, by osmosis, in the world – are on a dangerous slope. 2022 was marked by a fall in all indicators, with less money pumping into businesses and a collapse in unicorn creation. France is in a worrying situation, with a spectacular start in 2022, followed by a collapse throughout the year.

© / Art Press

But there is more worrying, warns Romain Serman, director of BPIfrance USA: “The famous LPs, those who feed venture capital upstream, are now asking firms to adventure to delay calls for funds, requiring that the portfolios be cleaned up first.” Translation: the valuations of companies will be revised downwards, and the weakest will be euthanized. will inevitably cascade on start-ups”, concludes the representative of BPIfrance in San Francisco.

A more optimistic view often heard is that the federal decision to save Silicon Valley Bank signals a major shift: the US government will support its tech sector “no matter what.” Because what is at stake is neither more nor less than the preservation of the economic supremacy of the United States, of which technological advance is the essential vector. This therefore means: negotiating the wave of artificial intelligence well; reforming a military-strategic complex to adapt it to geopolitical tensions; gradually disengage from China; monetize the response to the climate crisis, and ensure the effectiveness of the generous Biden plan, theInflation Reduction Act. Such pragmatism is worth a few sprains to liberalism, isn’t it?